How to Read a Balance Sheet Without Feeling Intimidated

A practical guide to understanding what a balance sheet shows, why it matters, and which numbers small business owners should pay attention to most.

FINANCIAL STATEMENTS

How to Read a Balance Sheet Without Feeling Intimidated

If you’ve ever looked at a balance sheet and thought, “I have no idea what I’m looking at,” you’re not alone.

Most small business owners hear a lot about the Profit & Loss report, but the balance sheet often gets less attention. That’s understandable. At first glance, it can feel more technical and less intuitive.

The good news is that a balance sheet does not have to feel intimidating. Once you understand what it measures, it becomes a useful tool for assessing your business's overall financial position.

What is a balance sheet?

A balance sheet is a financial report that shows what your business:

owns

owes

and what is left over for the owner

It gives you a snapshot of the business at a specific point in time.

While a Profit & Loss report shows performance over a period of time, a balance sheet shows financial position on a specific date.

The three main parts of a balance sheet

A balance sheet is built around three main categories:

1. Assets

Assets are things the business owns or controls that have value.

Common examples include:

bank account balances

accounts receivable

equipment

inventory

prepaid expenses

In simple terms, assets are the resources available to the business.

2. Liabilities

Liabilities are what the business owes.

Common examples include:

credit card balances

loans

unpaid bills

payroll liabilities

sales tax payable

These are the business’s obligations.

3. Equity

Equity is what remains after liabilities are subtracted from assets.

This generally reflects:

owner contributions

retained earnings

owner draws

cumulative profit left in the business

In simple terms, equity represents the owner’s financial interest in the business.

The basic balance sheet formula

At the heart of every balance sheet is this formula:

Assets = Liabilities + Equity

This is why it is called a balance sheet.

If the books are accurate, both sides should balance.

Why the balance sheet matters

Some business owners focus only on profit, which makes sense at first. But profit alone does not tell the whole story.

A balance sheet helps answer questions like:

How much cash does the business actually have?

How much debt is the business carrying?

Are customers slow to pay?

Are liabilities building up?

Is the business financially stable?

That is why this report matters. It adds context that a Profit & Loss report cannot provide on its own.

What to look at on your balance sheet

You do not need to analyze every line in detail each month. But there are a few areas worth reviewing regularly.

Cash

Your cash balances show how much money is currently available in business accounts.

This is one of the easiest places to start because it tells you what the business has on hand right now.

Accounts receivable

If you send invoices, this section shows money customers still owe you.

If receivables are growing too quickly, it may be a sign that:

invoices are not being paid promptly

follow-up is needed

cash flow could become tighter than expected

Loans and credit cards

These balances show what the business still owes.

Reviewing them regularly helps you keep an eye on:

rising debt

repayment progress

how much of your cash flow is tied to obligations

Owner’s equity

This section can help you understand how much value has built up in the business over time.

It can also show whether owner draws or losses affect the company's overall financial position.

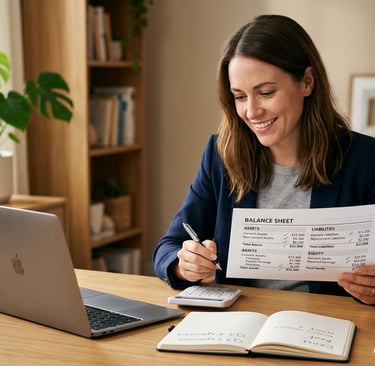

A simple example

Here is a very simplified example of what a balance sheet might show:

Assets

Cash: $18,000

Accounts Receivable: $4,500

Equipment: $7,000

Total Assets: $29,500

Liabilities

Credit Card Balance: $2,500

Business Loan: $8,000

Total Liabilities: $10,500

Equity

Owner’s Equity: $19,000

Total Liabilities + Equity: $29,500

This means the business has $29,500 in total assets, owes $10,500, and has $19,000 in owner equity.

Common balance sheet mistakes

Here are a few common issues that make balance sheets harder to trust:

Not reconciling accounts

If bank, credit card, or loan accounts are not reconciled, balance sheet numbers may be off.

Leaving old receivables on the books

If unpaid invoices are no longer collectible but still appear as assets, the report becomes misleading.

Recording owner activity incorrectly

Draws, contributions, and personal transactions can distort equity if they are not handled correctly.

Ignoring liabilities

Some business owners review income closely but forget to monitor tax liabilities, loans, or unpaid bills.

A practical way to use this report

If you want to keep things simple, review your balance sheet monthly and ask:

Do the cash balances look right?

Are receivables current?

Are liabilities increasing?

Are any balances unusual or unclear?

Does this report match what I know is happening in the business?

You do not need to become an accountant to get value from this report. You just need enough familiarity to spot what deserves a closer look.

Final thoughts

A balance sheet may seem less familiar than a Profit & Loss report, but it plays an important role in understanding the financial health of your business.

It helps you look beyond income and expenses to see:

what the business owns

what it owes

and how financially stable it is overall

Once you understand the basics, it becomes much easier to use.

Questions about your financial reports?

If you’d like help reviewing your balance sheet or understanding what your reports are showing, I’d be happy to help.